Top Non GamStop Casinos for UK Players

Roughly 20% of UK punters who self-excluded through GamStop still go on to play at offshore sites within twelve months — and if you're on this page, you already know which direction you're heading. Our team spent considerable time testing non gamstop casinos across licensing, payouts, game depth, and support response. What you'll find here are the ones that held up under scrutiny, not the ones that simply paid for placement.

We've ranked the best options UK players are actually using in 2026, then reviewed 5 in detail. Each review names real limitations — because a site with no flaws hasn't been tested properly. The offshore casino that suits a crypto punter looks nothing like the one that suits a £10-deposit casual player, so we've covered the spectrum.

Our Recommended Non GamStop Casinos Ranked

-

1

Very Well Casino 5.0/5100% + 50 Free Spins Bonus

Very Well Casino 5.0/5100% + 50 Free Spins Bonus -

2

BassWin Casino 4.7/5150% + 50 FS

BassWin Casino 4.7/5150% + 50 FS -

3

DonBet Casino 5.0/5150% + 50 FS Welcome Bonus

DonBet Casino 5.0/5150% + 50 FS Welcome Bonus -

4

GoldenBet Casino 4.9/5100% Welcome Bonus

GoldenBet Casino 4.9/5100% Welcome Bonus -

5

Patrick Spins Casino 5.0/5200% Welcome Bonus

Patrick Spins Casino 5.0/5200% Welcome Bonus -

6

MyStake Casino 4.7/5Get 150% Up to £1000

MyStake Casino 4.7/5Get 150% Up to £1000 -

7

Lucky Mister Casino 4.9/5150% Bonus

Lucky Mister Casino 4.9/5150% Bonus -

8

BetPortal Casino 4.6/5300% + 150 Free Spins

BetPortal Casino 4.6/5300% + 150 Free Spins -

9

Rivo Casino 4.9/51000% up to €10,000 + 25% cashback

Rivo Casino 4.9/51000% up to €10,000 + 25% cashback -

10

Wildies 4.7/5400% up to £3500 + 150 FS

Wildies 4.7/5400% up to £3500 + 150 FS -

11

CleanWins Casino 5.0/5200% up to £2000

CleanWins Casino 5.0/5200% up to £2000 -

12

CasinOK 4.8/5300% + 200 FS

CasinOK 4.8/5300% + 200 FS -

13

Mad Casino 4.8/5200% Bonus

Mad Casino 4.8/5200% Bonus -

14

Cash Lounge Casino 4.9/5525% UP TO £3,000 + 350 FS

Cash Lounge Casino 4.9/5525% UP TO £3,000 + 350 FS -

15

VibroBet 4.7/5225% + 210 Free Spins

VibroBet 4.7/5225% + 210 Free Spins -

16

Zombillion Casino 4.9/5250% up to £4000 + 200 FS

Zombillion Casino 4.9/5250% up to £4000 + 200 FS -

17

Betmica Casino 4.9/5570% up to £5700 + 270 FS

Betmica Casino 4.9/5570% up to £5700 + 270 FS -

18

Night Luck Casino 4.9/5805% up to £6400 + 280 FS

Night Luck Casino 4.9/5805% up to £6400 + 280 FS -

19

Casper Bets 4.9/5500% UP TO £3,500 + 300 FS

Casper Bets 4.9/5500% UP TO £3,500 + 300 FS -

20

Crown Jewelz Casino 4.9/5200% up to £1000 + 50 FS

Crown Jewelz Casino 4.9/5200% up to £1000 + 50 FS -

21

Jet Set Spins 4.9/5700% Welcome Bonus + 375 Wagerless Free Spins

Jet Set Spins 4.9/5700% Welcome Bonus + 375 Wagerless Free Spins -

22

Reel Raven Casino 4.9/5250% up to 3000 + 100 FS

Reel Raven Casino 4.9/5250% up to 3000 + 100 FS -

23

BetRide Casino 4.8/5425% Casino Welcome Bonus

BetRide Casino 4.8/5425% Casino Welcome Bonus -

24

Winner Island Casino 5.0/5£1,000 and 100 FS in Big Bass Bonanza

Winner Island Casino 5.0/5£1,000 and 100 FS in Big Bass Bonanza -

25

Bloody Slots 4.9/5600% + 450 Wagerless Free Spins

Bloody Slots 4.9/5600% + 450 Wagerless Free Spins -

26

Slim King Casino 4.9/5100% up to £1000 + 200 FS

Slim King Casino 4.9/5100% up to £1000 + 200 FS -

27

Rolletto Casino 4.8/5150% + 50 FS Bonus

Rolletto Casino 4.8/5150% + 50 FS Bonus -

28

Pirate Pots Casino 4.9/5250% UP TO 3000 + 100FS

Pirate Pots Casino 4.9/5250% UP TO 3000 + 100FS -

29

CasinoJoy 4.7/5450% Bonus + 425 Free Spins

CasinoJoy 4.7/5450% Bonus + 425 Free Spins -

30

Megaways VIP 4.5/5400% First Deposit Bonus

Megaways VIP 4.5/5400% First Deposit Bonus -

31

Velobet Casino 4.9/5150% + 70 FS Bonus

Velobet Casino 4.9/5150% + 70 FS Bonus -

32

CosmoBet Casino 4.9/5200% Up to $1500

CosmoBet Casino 4.9/5200% Up to $1500 -

33

Jettbet Casino 4.8/5200% + 100 Free Spins Bonus

Jettbet Casino 4.8/5200% + 100 Free Spins Bonus -

34

BetNjet 4.4/5120% up to £200 + 100 FS

BetNjet 4.4/5120% up to £200 + 100 FS -

35

Forza Bet 4.5/550% Welcome Bonus

Forza Bet 4.5/550% Welcome Bonus -

36

Lucky Barry Casino 5.0/5100% Bonus on First Deposit

Lucky Barry Casino 5.0/5100% Bonus on First Deposit -

37

Great Slots 4.2/5Get Up To €2500 + 10% Weekly Cashback

Great Slots 4.2/5Get Up To €2500 + 10% Weekly Cashback -

38

Kingdom Casino 4.3/5100% up to £2.000

Kingdom Casino 4.3/5100% up to £2.000 -

39

Richy Leo Casino 4.9/5x1 Wager 10% Bonus + 10FS

Richy Leo Casino 4.9/5x1 Wager 10% Bonus + 10FS -

40

FreshBet Casino 4.8/5100% On First Deposit

FreshBet Casino 4.8/5100% On First Deposit -

41

Bounty Reels Casino 4.9/5150% To Your First Deposit!

Bounty Reels Casino 4.9/5150% To Your First Deposit! -

42

Lucky Carnival Casino 4.9/5100% Deposit Match

Lucky Carnival Casino 4.9/5100% Deposit Match -

43

Wino Casino 4.6/5200% up to £500

Wino Casino 4.6/5200% up to £500 -

44

Koi Spins Casino 5.0/5200% Deposit Bonus

Koi Spins Casino 5.0/5200% Deposit Bonus -

45

Bet Ninja 4.2/5100% Bonus Up to £100

Bet Ninja 4.2/5100% Bonus Up to £100 -

46

Tropical Wins Casino 5.0/5150% Initial Offer

Tropical Wins Casino 5.0/5150% Initial Offer -

47

Rollino Casino 5.0/5Welcome Bonus 450% Up To €6,000

Rollino Casino 5.0/5Welcome Bonus 450% Up To €6,000 -

48

Sweety Win Casino 4.9/510% No Wager Bonus + 10 Free Spins

Sweety Win Casino 4.9/510% No Wager Bonus + 10 Free Spins -

49

Lucky Manor Casino 5.0/5100-200 FS On Deposit

Lucky Manor Casino 5.0/5100-200 FS On Deposit -

50

Fire Scatters Casino 5.0/5175% Deposit Bonus

Fire Scatters Casino 5.0/5175% Deposit Bonus -

51

Richy Fox Casino 5.0/5175% Welcome Deal

Richy Fox Casino 5.0/5175% Welcome Deal -

52

Tropicanza Casino 4.9/5100% Deposit Bonus

Tropicanza Casino 4.9/5100% Deposit Bonus -

53

BigWinBox Casino 5.0/5100% Match On First 3 Deposits

BigWinBox Casino 5.0/5100% Match On First 3 Deposits -

54

Hand of Luck Casino 5.0/510% and 10FS with x1 Wager

Hand of Luck Casino 5.0/510% and 10FS with x1 Wager -

55

Richy Farmer Casino 5.0/5100 FS Bonus

Richy Farmer Casino 5.0/5100 FS Bonus -

56

SlotoNauts Casino 5.0/5175% Match Up To €1000

SlotoNauts Casino 5.0/5175% Match Up To €1000 -

57

Professor Wins Casino 4.9/5100% On First 3 Deposits

Professor Wins Casino 4.9/5100% On First 3 Deposits -

58

Yummy Wins Casino 5.0/512% Fist Deposit Bonus With x1 Wager

Yummy Wins Casino 5.0/512% Fist Deposit Bonus With x1 Wager -

59

Slots Muse Casino 5.0/5100-200 Free Spins On Deposit

Slots Muse Casino 5.0/5100-200 Free Spins On Deposit -

60

Bonus Strike Casino 5.0/5100% Bonus + 725FS Package

Bonus Strike Casino 5.0/5100% Bonus + 725FS Package -

61

Twinky Win Casino 4.6/5100-200 Free Spins On Deposit

Twinky Win Casino 4.6/5100-200 Free Spins On Deposit -

62

PH Casino 4.7/5Up to £500 Bonus

PH Casino 4.7/5Up to £500 Bonus -

63

Richy Fish Casino 5.0/5200% Bonus Offer

Richy Fish Casino 5.0/5200% Bonus Offer -

64

Hawaii Spins Casino 5.0/5200% Welcome Bonus

Hawaii Spins Casino 5.0/5200% Welcome Bonus -

65

Papaya Wins Casino 5.0/5175% Offer On 1st Deposit

Papaya Wins Casino 5.0/5175% Offer On 1st Deposit -

66

Rabbit Win Casino 5.0/5100 FS On First Deposit

Rabbit Win Casino 5.0/5100 FS On First Deposit -

67

Jimmy Winner Casino 5.0/5150% Offer On First Deposit

Jimmy Winner Casino 5.0/5150% Offer On First Deposit -

68

VooDoo Wins Casino 5.0/5175% Bonus

VooDoo Wins Casino 5.0/5175% Bonus -

69

Jammy Jack Casino 5.0/5150% Match On 1st Deposit

Jammy Jack Casino 5.0/5150% Match On 1st Deposit -

70

Twister Wins Casino 5.0/5525% Bonus Package

Twister Wins Casino 5.0/5525% Bonus Package -

71

Richy Reels Casino 5.0/5175% For First Deposit

Richy Reels Casino 5.0/5175% For First Deposit -

72

Yeti Win Casino 5.0/512% Bonus With x1 Wagering

Yeti Win Casino 5.0/512% Bonus With x1 Wagering -

73

Shiny Joker Casino 4.6/520-60% Bonus

Shiny Joker Casino 4.6/520-60% Bonus -

74

Top G Casino 4.7/5100% + 100 FS Bonus Offer

Top G Casino 4.7/5100% + 100 FS Bonus Offer -

75

Raptor Wins Casino 5.0/5175% First Deposit Bonus

Raptor Wins Casino 5.0/5175% First Deposit Bonus -

76

Scarab Wins Casino 5.0/5x1 Wager 10% Bonus

Scarab Wins Casino 5.0/5x1 Wager 10% Bonus -

77

Spin My Win Casino 5.0/512-17% Bonus With x1 Wager

Spin My Win Casino 5.0/512-17% Bonus With x1 Wager -

78

Slots Shine Casino 5.0/5150% On First Deposit

Slots Shine Casino 5.0/5150% On First Deposit -

79

Euphoria Wins Casino 5.0/5200% Deposit Offer

Euphoria Wins Casino 5.0/5200% Deposit Offer -

80

Amigo Wins Casino 5.0/5150% Bonus On Deposit

Amigo Wins Casino 5.0/5150% Bonus On Deposit -

81

Fancy Reels Casino 5.0/5175% Deposit Match

Fancy Reels Casino 5.0/5175% Deposit Match -

82

Hustles Casino 4.7/5100% Bonus Up To $1000

Hustles Casino 4.7/5100% Bonus Up To $1000 -

83

Kaboom Slots Casino 5.0/5450% Bonuses On 3 Deposits

Kaboom Slots Casino 5.0/5450% Bonuses On 3 Deposits -

84

Orion Spins Casino 5.0/510% On Deposit & 10 Free Spins

Orion Spins Casino 5.0/510% On Deposit & 10 Free Spins -

85

Agent noWager Casino 4.9/5Welcome Bonuses Up To €3000 With x1 Wager

Agent noWager Casino 4.9/5Welcome Bonuses Up To €3000 With x1 Wager -

86

Casiroom Casino 4.9/550% Bonus + 125FS

Casiroom Casino 4.9/550% Bonus + 125FS -

87

CasiGood Casino 5.0/5200% On First Deposit

CasiGood Casino 5.0/5200% On First Deposit -

88

Fortune Clock Casino 4.7/5225% Deposit Bonus + 225 Free Spins

Fortune Clock Casino 4.7/5225% Deposit Bonus + 225 Free Spins -

89

Tropic Slots Casino 5.0/5525% Bonus Packages For All

Tropic Slots Casino 5.0/5525% Bonus Packages For All -

90

Milky Wins Casino 5.0/510% Bonus With Only x1 Wager

Milky Wins Casino 5.0/510% Bonus With Only x1 Wager -

91

Plexian Casino 4.8/5100% Welcome Bonus

Plexian Casino 4.8/5100% Welcome Bonus -

92

Pyramid Spins Casino 4.9/5450% Deposit Package Up To €3000

Pyramid Spins Casino 4.9/5450% Deposit Package Up To €3000 -

93

PlayHub Casino 4.6/5100% Welcome Bonus

PlayHub Casino 4.6/5100% Welcome Bonus -

94

God Odds Casino 4.8/550 FS + 100% Deposit Bonus

God Odds Casino 4.8/550 FS + 100% Deposit Bonus -

95

BetSwagger Casino 4.5/5100% Match Up To $500

BetSwagger Casino 4.5/5100% Match Up To $500 -

96

Jackpot Charm Casino 4.8/5450% Welcome Package

Jackpot Charm Casino 4.8/5450% Welcome Package -

97

Captain Marlin Casino 5.0/5475% Up To €3000

Captain Marlin Casino 5.0/5475% Up To €3000

Velobet Casino

With 6,000 slots on offer, Velobet sits at the heavier end of non gamstop casinos for volume-focused players who want depth beyond the usual few hundred titles.

| Licence | Curacao (OGL/2024/1798/1048) |

|---|---|

| Welcome | 150% up to £500 |

| Wagering | 30x (deposit + bonus) |

| Min deposit | £20 |

| Withdrawal | £20 / 1-3 business days |

| Games | 7,000 total — 6,000 slots, 200 live tables |

| Payment | Visa, Mastercard, Skrill, Neteller, Paysafecard |

| Providers | Pragmatic Play, Evolution, Play'n GO, NetEnt |

| Devices | Mobile-optimized site (no dedicated app) |

The 30x playthrough on the welcome offer is genuinely manageable for slots not on gamstop at this scale, and VIP cashback carries zero wagering, which is a rare find among non gamstop sites. Lucky Streak and Iconic 21 power a live lobby that stretches to 200 tables, including game show titles like Monopoly Live and Dream Catcher.

Pros

- 7,000 games across slots and live tables

- VIP cashback with no wagering requirement

- Crypto deposits and withdrawals supported

- 30x wagering — below the offshore average

Cons

- Crypto welcome bonus wagered at 35x, not 30x

- No dedicated mobile app

Velobet suits high-volume slot players who want a non gamstop casino with a serious game library and a workable bonus structure.

Rolletto Casino

Rolletto stands apart from the other sites in this set by combining a non gamstop casino offer with sports, esports, and virtual sports under one licence, which means switching between a slot session and a live accumulator bet requires no separate account.

| Licence | Curacao (OGL/2024/1798/1048) |

|---|---|

| Founded | 2020 |

| Welcome | 150% up to £500 |

| Wagering | 40x (deposit + bonus) |

| Min deposit | £10 |

| Withdrawal | £20 / 1-3 business days |

| Games | 4,500 slots, 200 live tables |

| Payment | Visa, Mastercard, Bitcoin, Tether, Ethereum |

| Providers | NetEnt, Play'n GO, Pragmatic Play, Evolution |

| Devices | Mobile-optimized site (no dedicated app) |

The game library runs to 6,000 titles across providers like Nolimit City, Hacksaw, and Red Tiger, which gives slot races genuine variety rather than the same 50 titles recycled. For players exploring casinos outside GamStop with a crypto preference, instant Bitcoin payouts sidestep the 1-3 business day window that applies to card withdrawals.

Pros

- Instant Bitcoin withdrawals available

- Sports, esports, and virtuals on one account

- £10 minimum deposit keeps entry low

- 6,000 games across 10 named providers

Cons

- 40x wagering on the welcome bonus is above average

- No dedicated mobile app

Rolletto fits the punter who wants a single account to cover casino play, sports betting, and crypto cashouts without juggling multiple sites.

MyStake Casino

Depth of library is what MyStake leads with, stacking 4,600 titles alongside a crypto cashback programme that makes it one of the more rewarding non gamstop casinos for players who keep a crypto wallet handy.

| Licence | Curacao (OGL/2024/250/0115) |

|---|---|

| Welcome | 150% up to £750 |

| Wagering | 30x (deposit + bonus, slots only, 30 days) |

| Min deposit | £20 |

| Withdrawal | £20 / 1-3 business days |

| Games | 4,600 slots, 150 live tables |

| Payment | Visa, Mastercard, Skrill, Neteller, Bitcoin |

| Providers | Pragmatic Play, Evolution, Play'n GO, Hacksaw |

| Devices | Mobile-optimized site (no dedicated app) |

The 30x wagering requirement clears faster than most comparable operators in this set, and the provider lineup - Nolimit City, Relax Gaming, and Microgaming alongside the bigger names - means the catalogue has genuine range rather than 4,600 copies of the same slot template. Esports betting and virtual sports sit alongside the casino, so punters who switch between markets don't need a second account.

Pros

- Crypto cashback programme with multiple coin options

- 30x wagering - reasonable for this market

- Esports and virtual sports alongside casino

- 24/7 live chat available

Cons

- Max £5 bet during wagering is restrictive

- No dedicated mobile app

MyStake suits crypto-active punters who want a large slot library and the option to bet on esports without juggling separate accounts.

Very Well Casino

A tiered free spins welcome package built around classic Novomatic titles gives Very Well Casino a character that separates it cleanly from the other non gamstop casinos in this set, none of which lean so deliberately into the nostalgia slot catalogue.

| Licence | Anjouan Gaming (ALSI-202505022-FI1) |

|---|---|

| Founded | 2020 |

| Welcome | Up to 125 Free Spins across 5 deposits |

| Wagering | 35x on free spin winnings, max stake £2, valid 7 days |

| Min deposit | £20 |

| Withdrawal | £150 minimum / 24-48 hours (crypto instant, cards 1-3 business days) |

| Games | 3,000 total (2,500 slots, 150 live tables) |

| Payment | Visa, Mastercard, Bitcoin, Tether (USDT), Bank Transfer |

| Providers | Novomatic, NetEnt, Play'n GO, Pragmatic Play |

| Devices | Android APK download, responsive mobile site |

The 3,000-title library pulls from 9 named studios, with Yggdrasil and Push Gaming alongside the bigger names giving the slots catalogue more range than the headline figure alone suggests. Crypto withdrawals clear instantly, which puts it ahead of card-only routes that run to 3 business days.

Pros

- Crypto withdrawals processed instantly

- Low £20 minimum deposit

- Android APK available for download

- Sportsbook alongside casino in one account

Cons

- £150 minimum withdrawal is steep

- 35x wagering with a £2 max stake restricts bonus value

Very Well Casino suits the casual punter who enjoys classic slot titles and wants crypto flexibility without committing large sums to withdrawals.

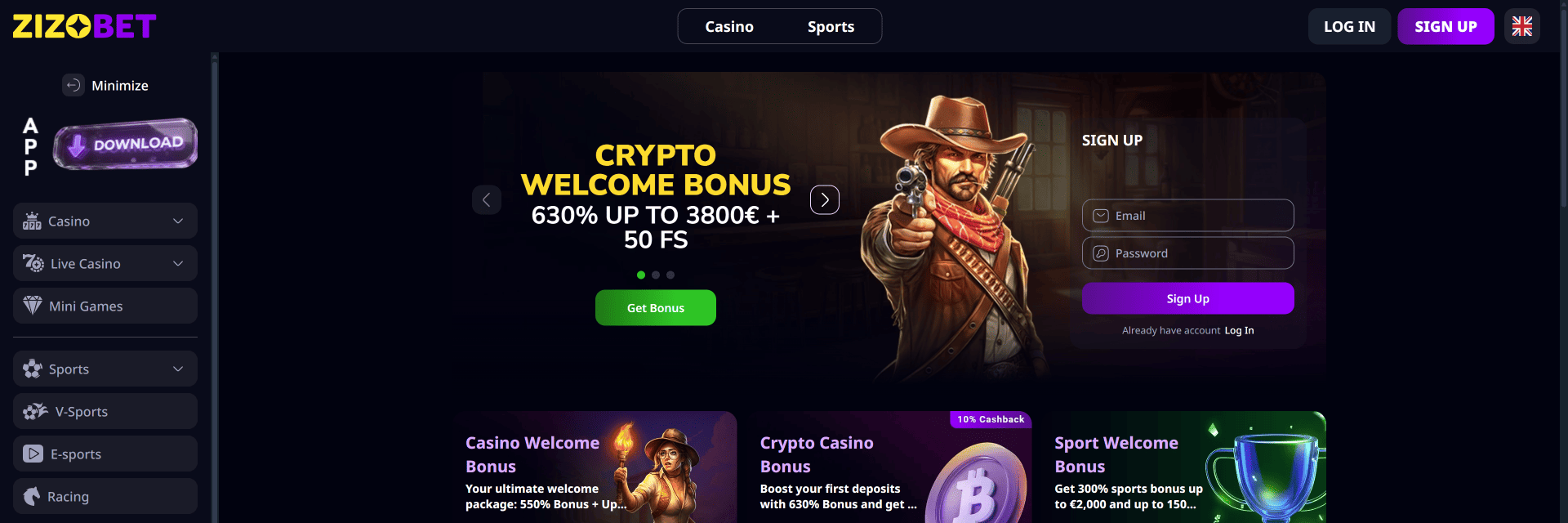

ZizoBet

That 550% welcome package puts ZizoBet at the aggressive end of non gamstop casinos, and with 8,000 titles spread across 6 major providers, the library backs up the headline figure rather than hiding behind it.

| Licence | Curacao Gaming Authority (CGA) — OGL/2024/1798/1048 |

|---|---|

| Welcome | Up to 550% Bonus + 50 Free Spins |

| Wagering | 30x (bonus + deposit) |

| Min deposit | £10 |

| Withdrawal | £20 / 1-3 banking days |

| Games | 6,500 slots, 247 live tables |

| Payment | Visa, Mastercard, Skrill, Neteller, Apple Pay |

| Providers | Pragmatic Play, Play'n GO, Evolution, Hacksaw Gaming |

| Devices | Mobile browser-first |

The 247 live tables run on Evolution, which means the quality floor is high even if the sportsbook is what ZizoBet clearly considers its second pillar. Crypto deposits process faster than the 1-3 banking day window quoted for fiat, making the site a reasonable fit for players who mix card and crypto withdrawals.

Pros

- 550% welcome bonus, low £10 entry point

- Crypto and fiat withdrawals both supported

- 247 live tables via Evolution

- 24/7 support and VIP Club included

Cons

- Max withdrawal capped at €100 on no-deposit offers

- Not integrated with GamStop self-exclusion

ZizoBet suits bonus hunters who also want a sportsbook on the same account, particularly those comfortable using crypto to speed up cashouts.